![]()

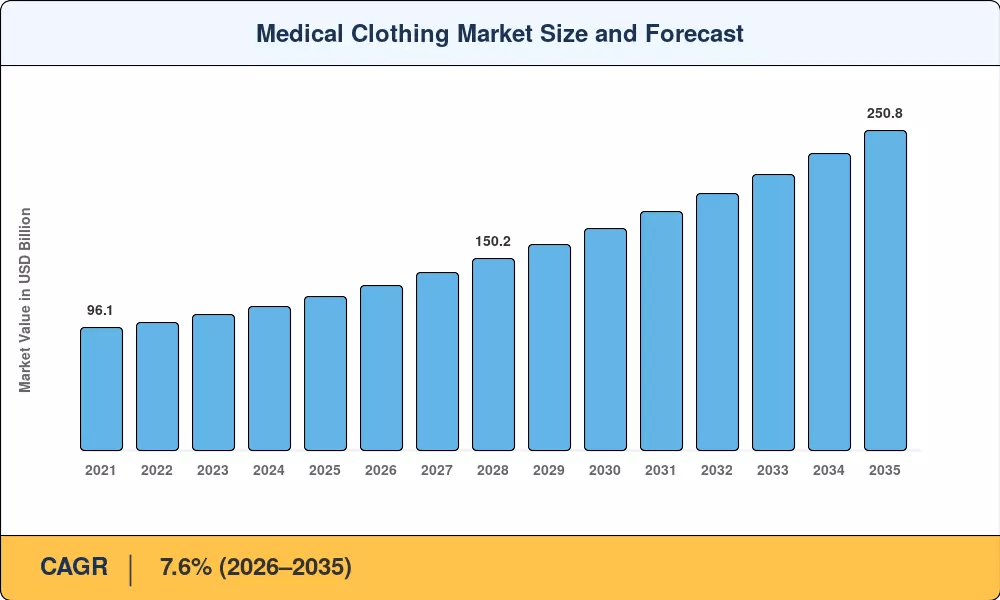

Medical Clothing Market to Surge from USD 129.7 Bn in 2026 to USD 250.8 Bn by 2035—Powered by Rising Infection-Prevention Regulations, Smart-Textile Innovation

NY, CA, UNITED STATES, June 19, 2026 /EINPresswire.com/ — As per Market Research Future, the global Medical Clothing Market size to reach USD 250.8 Billion by 2035 from USD 129.7 Billion in 2026, at a CAGR of 7.6% during the forecast period 2026–2035. The market base was estimated at USD 120.5 Billion in 2025.

The 7.6% CAGR—anchored by structural healthcare infrastructure demand rather than discretionary spending—is driven by three converging forces: rising global hospital-acquired infection (HAI) prevention mandates that continue to tighten barrier-performance benchmarks for clinical garments, sustained smart-textile and sensor-embedded apparel innovation that is bridging clinical wear and remote patient monitoring, and a sustained wave of public investment in hospital capacity and ambulatory surgical center expansion that is converting medical clothing procurement from a cost center into a compliance-grade priority.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/26704

Key Market Trends & Growth Drivers

Rising Infection-Prevention Regulations and Updated WHO Barrier Standards

In the United States, the CDC estimates that hospital-acquired infections add roughly USD 28.4 billion in annual treatment costs, giving administrators a quantifiable return-on-investment rationale for higher-specification clinical apparel. These compliance pressures convert what could be discretionary procurement into a regulatory baseline, insulating disposable gown demand from budget-cycle downturns.

Level 3 gowns are now the WHO-recommended minimum for any procedure involving moderate fluid exposure. Specifying Level 3 as the procurement floor reduces HAI liability and aligns with updated global standards. Each percentage point of regulatory tightening translates into measurable prescription volume for barrier-rated clinical apparel, and the infection-prevention apparel schedule embedded in routine healthcare operations makes this driver structurally durable through 2035.

Ambulatory Surgical Center Expansion and Outpatient Migration

Legacy inpatient-only surgical models, long the default care setting, are giving ground to ambulatory surgery center case volumes that rose 9.3% year-over-year in 2024 in the United States, with orthopedic and ophthalmic procedures shifting out of hospital operating rooms at the fastest rate in a decade. Medicare’s 2025 rule expanding the list of ASC-covered procedures by 14 CPT codes further accelerates this trend.

Each additional outpatient case creates incremental demand for single-use gowns, drapes, and scrub sets, expanding the Medical Clothing Market without proportional growth in inpatient bed counts. The convergence of diagnostic scheduling with therapeutic apparel procurement is creating a demand loop that personalizes clinical garment supply at scale.

Smart-Textile Innovation and Sensor-Embedded Clinical Wear

Legacy cotton-polyester blends that offered comfort but limited fluid resistance are giving way to polypropylene SMS laminates engineered for high-barrier surgical environments, while a newer class of sensor-embedded textiles is bridging clinical wear and remote patient monitoring. Clinical trials at Johns Hopkins and Singapore General Hospital have shown that scrubs integrated with micro-sensor arrays can continuously send heart rate, respiration rate, and skin temperature to electronic health records with 96% accuracy.

The investment in medical-grade wearable textiles by venture capitalists increased to USD 480 million in 2024, threefold the USD 160 million in 2021. If the time to get regulatory clearance is shorter—the FDA’s De Novo pathway accepted two sensor-scrub applications late in 2024—sensor-integrated garments could move from pilot programs into standard procurement lists in three to four years, igniting a premium segment of the Medical Clothing Market.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/26704

Market Segment Insights

BY PRODUCT TYPE

Surgical Gowns: Dominant segment with ~34.0% revenue share in 2024. Reflecting entrenched regulatory compliance with AAMI and EN 13795 barrier standards. Surgical gowns, available across Level 1 through Level 4 classifications, anchor institutional formularies globally due to their mandatory use in every invasive procedure and decades of clinical evidence supporting infection-prevention protocols.

Hospital procurement teams treat them as default first-line apparel, and standardized pricing has enabled broad adoption even in cost-sensitive emerging markets.

BY USABILITY

Disposable: Dominant segment with 9.1% CAGR (2026–2035). Driven by single-use infection-control mandates across the Medical Clothing Market. Disposable garments dominate procurement volume because single-use protocols eliminate cross-contamination risk and simplify sterile processing workflows. Hospital procurement teams treat disposable gowns as default first-line apparel, and standardized pricing has enabled broad adoption even in cost-sensitive emerging markets.

Reusable: 4.8% CAGR (2026–2035). Circular-economy pilots and sustainability mandates drive demand in Nordic and Western European markets. Reusable systems are gaining renewed attention where circular-textile infrastructure exists, particularly in markets with government co-funded collection and fiber-recovery programs. The Medical Clothing Market will likely sustain a dual-track model, with disposables prevailing in high-acuity settings and reusables gaining ground in non-sterile, routine-care environments.

BY END USER

Hospitals: Dominant end user with ~60.2% revenue share in 2024. Comprehensive oncology service lines and high procedure volumes dominate volume. Hospitals remain the primary delivery site for medical clothing due to concentrated procedure volumes and formalized group purchasing organization contracts.

Ambulatory Surgical Centers: Fastest-growing end-user segment at 7.8% CAGR (2026–2035). Outpatient migration and cost optimization drive demand as disposable apparel reduces the need for supervised sterile processing. ASCs and community clinics increasingly prescribe single-use medical clothing options to manage central sterile processing capacity.

BY MATERIAL

Polypropylene SMS: Dominant material with ~41.7% revenue share in 2024. Barrier performance and cost efficiency anchor institutional procurement globally. Polypropylene SMS leads material selection in the Medical Clothing Market because it delivers the best balance of fluid resistance, breathability, and manufacturing cost for single-use applications.

Cotton & Cotton Blends: USD 14.2 Billion in 2025. Comfort and reusable program compatibility sustain demand in non-sterile and routine-care environments.

BY DISTRIBUTION CHANNEL

Direct Institutional Procurement: Dominant channel with ~57.8% revenue share in 2024. GPO and IDN contracts dominate volume, channeling routine medical clothing supply. Large hospital systems and IDNs negotiate multi-year contracts through group purchasing organizations, locking in pricing and supply continuity. GPO-negotiated agreements typically deliver 15–25% discounts off list price by aggregating demand across member hospitals.

Distributors & Wholesalers: USD 26.3 Billion in 2025. Breadth of SKU coverage and regional logistics capability sustain demand.

E-Commerce Platforms: Fastest-growing distribution channel at 16.3% CAGR (2026–2035). Small-provider access and digital procurement convenience drive demand. E-commerce platforms are expanding access for independent clinics, physician offices, and home-health agencies that lack GPO membership. Subscription models that guarantee replenishment cycles give suppliers predictable demand signals and reduce channel intermediary costs.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/medical-clothing-market-26704

Regional Outlook

North America — Dominant Market (~41.0% Share, 2025)

The United States generates approximately 72.3% of North American Medical Clothing Market revenue, driven by the FDA device classification rules, commercial insurance coverage of barrier-rated apparel as first-line infection prevention, and broad reimbursement for disposable gown regimens—a single policy ecosystem that converted a commodity-dominated market into one with a structural compliance-grade tail. CMS reimbursement for surgical supplies under the hospital outpatient prospective payment system has driven adoption in academic medical centers, while community oncology networks increasingly prescribe single-use medical clothing options to manage sterile processing capacity. The US dominates through a combination of high per-patient spending, robust payer coverage, and rapid smart-textile adoption.

Europe — Second Largest (28.5% Share, 2025)

Europe’s Medical Clothing Market reflects divergent national strategies—Germany leads regionally with advanced nonwoven manufacturing capacity, contributing 23.8% of regional share, while the UK historically used selective procurement targeting before broadening coverage through NHS Supply Chain restructuring at 7.2% CAGR. France contributes ~18.5% of regional share through hospital-at-home programs. Italy contributes 12.6% of regional share on surgical volume recovery. Spain is growing at 6.9% CAGR on public hospital investment.

Asia-Pacific — Fastest-Growing Region (10.5% CAGR, 2026–2035)

Asia-Pacific is the engine of the Medical Clothing Market. China holds the largest regional share with ~38.2% of regional revenue, driven by vertically integrated nonwoven production clusters in Hubei and Zhejiang provinces. India is growing at 12.1% CAGR on the back of Ayushman Bharat bed expansion. Japan contributes USD 4.6 Billion through aging population and long-term care demand at steady pace. South Korea is growing at 9.4% CAGR on smart-hospital initiatives.

Middle East & Africa — Emerging Opportunity (3.4% Share, 2025)

The Middle East & Africa is bifurcated between well-funded Gulf states and resource-constrained Sub-Saharan nations. Saudi Arabia leads the region with Vision 2030 healthcare cluster development, contributing ~28.4% of regional share—NEOM health cluster and the UAE’s Cleveland Clinic and Mayo Clinic affiliations have created pockets of excellence for medical clothing procurement. The UAE is growing at 8.9% CAGR on medical tourism and premium facilities. South Africa contributes USD 0.6 Billion on public health reform.

South America — Growing Presence (USD 5.8 Billion, 2025)

Brazil anchors South America’s Medical Clothing Market at ~52.1% of regional revenue, with the Unified Health System (SUS) incorporating standardized disposable surgical kits into the national healthcare protocol, providing a stable demand floor that smooths regional forecasts. Access to premium barrier-rated apparel remains limited by import dependencies, though the Brazilian textile industry has initiated domestic nonwoven production feasibility studies. Argentina is growing at 6.4% CAGR on private clinic expansion.

Competitive Landscape and Recent Developments

The Medical Clothing Market exhibits medium concentration, with the top five companies collectively holding an estimated 32–38% of global revenue. The Herfindahl-Hirschman Index sits below 1,000, indicating a fragmented competitive structure where regional and specialty players retain meaningful share alongside multinational conglomerates. Competition increasingly pivots on material innovation, digital procurement capability, and sustainability credentials rather than price alone.

The competitive landscape is stratified between vertically integrated U.S. manufacturers serving global medical clothing markets, premium barrier-performance specialists capturing high-acuity tenders, and direct-to-consumer lifestyle brands consolidating the branded scrub segment.

KEY COMPANIES AND RECENT MILESTONES

Medline Industries (December 2025): Successfully priced and finalized the largest initial public offering (IPO) of the year, listing on the Nasdaq at USD 29 per share, raising over USD 6.2 billion in fresh capital and valuing the medical supply giant at over USD 37 billion. Vertically integrated U.S. manufacturer with surgical gowns, procedure packs, and scrubs, commanding ~8–11% of global Medical Clothing Market revenue.

Cardinal Health (2024–2025): Maintains leadership with disposable gowns, drapes, and sterilization wraps, leveraging distribution-scale advantage, holding ~6–9% of global revenue. Premium positioning in specialty segments offsets price compression in competitive markets.

Mölnlycke Health Care (June 2026): Expanded the market penetration of its premium BARRIER® surgical gown and custom procedure tray (CPT) lines, utilizing advanced polymer configurations engineered to strictly balance fluid repellency with breathability across high-fluid operating room environments. Premium barrier-performance focus anchors a strong global franchise, holding ~5–7% of global revenue.

Future Outlook: 2026–2035

By 2030, precision sensor-embedded clinical wear will become the operating system of medical clothing management. The convergence of companion diagnostics and targeted sensor technology will reshape the Medical Clothing Market through the late 2020s. By 2030, an estimated 40% of newly equipped hospital units will deploy sensor-integrated scrub systems for continuous vital-sign monitoring, creating a diagnostic-therapeutic apparel revenue loop.

Machine-learning models that integrate usage, wear-pattern, and compliance data can recommend optimal procurement sequencing of disposable gowns, reusable scrubs, and smart textiles for individual facilities. Start-ups have raised over USD 800 million in venture funding for healthcare decision-support tools since 2023.

Circular-textile business models and AI-integrated clinical decision support will reframe cost structures by the early 2030s. The EU aims to ensure that all textiles placed on its market are recyclable or compostable by 2030. Medical textiles currently fall under a partial exemption, but policymakers have signaled that exemptions will narrow by 2032. Manufacturers investing in mono-polymer construction and chemical-recycling partnerships today will secure first-mover advantage as regulations tighten.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/medical-protective-clothing-market-30903

https://www.marketresearchfuture.com/reports/surgical-drapes-and-gowns-market-7122

https://www.marketresearchfuture.com/reports/personal-protective-equipment-market-3826

https://www.marketresearchfuture.com/reports/biomedical-textiles-market-6079

https://www.marketresearchfuture.com/reports/medical-smart-textile-market-1123

https://www.marketresearchfuture.com/reports/infection-control-market-5901

https://www.marketresearchfuture.com/reports/wound-dressing-market-21740

https://www.marketresearchfuture.com/reports/hospital-supplies-market-42944

https://www.marketresearchfuture.com/reports/disposable-medical-supplies-market-43214

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery