![]()

Insulin Syringes Market to Surge from USD 1.99B in 2026 to USD 3.00B by 2035—Powered by Rising Global Diabetes Prevalence, Safety-Engineered Syringe Mandates

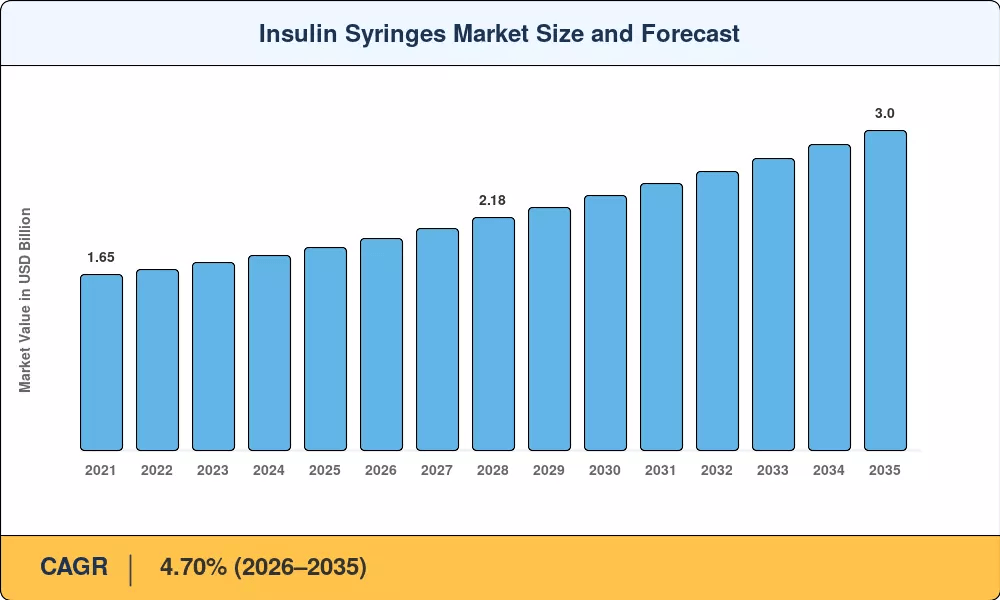

NY, CA, UNITED STATES, June 25, 2026 /EINPresswire.com/ — As per Market Research Future, the global Insulin Syringes Market size to reach USD 3.00 Billion by 2035 from USD 1.99 Billion in 2026, at a CAGR of 4.70% during the forecast period 2026–2035. The market base was estimated at USD 1.90 Billion in 2025.

The 4.70% CAGR—anchored by structural diabetes demand rather than discretionary healthcare spending—is driven by three converging forces: the International Diabetes Federation’s projection of 643 million adults living with diabetes by 2030, which ensures a durable multi-decade consumable cycle for every newly diagnosed insulin-dependent patient; safety-engineered and low dead-space syringe mandates that continue to widen the addressable base while increasing average selling prices by 30–50% per unit; and the persistent cost advantage of syringes over insulin pens and pumps in low- and middle-income countries where out-of-pocket spending dominates healthcare financing.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/12070

Key Market Trends & Growth Drivers

Rising Global Diabetes Prevalence and Expanding Insulin-Dependent Populations

The IDF Diabetes Atlas 10th Edition documents 537 million adults with diabetes in 2021, a figure projected to reach 643 million by 2030 and 783 million by 2045. Each newly diagnosed insulin-dependent patient enters a multi-decade consumable cycle, requiring 3–4 syringes daily in intensive regimens.

This demographic engine operates independently of technology substitution trends, giving the Insulin Syringes Market a durable demand floor that few medical disposable categories enjoy. Type 2 diabetes accounts for over 90% of all diabetes cases globally, while Type 1 patients, though fewer in number, use insulin from diagnosis and inject 4–6 times daily under intensive regimens, generating higher per-patient syringe consumption and driving the segment’s faster growth rate at 5.50% CAGR.

Safety-Engineered Syringe Mandates and Low Dead-Space Technology Adoption

OSHA’s Bloodborne Pathogens Standard requires U.S. healthcare employers to evaluate and implement safer sharps devices annually. Compliance drives a rolling upgrade cycle from conventional to retractable-needle and shielded-needle syringes, increasing average selling prices by 30–50% per unit.

The EU’s equivalent Sharps Directive has produced similar conversion patterns across member states, and these mandates sustain premium-tier growth within the Insulin Syringes Market. Low dead-space syringes retain less than 2 units of residual insulin per injection versus 5+ units in conventional designs, translating to 10–15% insulin savings per patient annually.

Cost Advantage Over Pens and Pumps and Emerging-Market Volume Expansion

A standard 100-count box of U-100 insulin syringes retails below USD 15 in most U.S. pharmacies, whereas a monthly pen needle supply runs USD 40–75 and insulin pump consumables exceed USD 300 per month.

In low- and middle-income countries where out-of-pocket spending dominates healthcare financing, this price differential makes syringes the only economically viable delivery method for the majority of insulin users, reinforcing unit volume growth in the Insulin Syringes Market. Patent expirations on major insulin analogs between 2024 and 2028 are expected to introduce 15–20 biosimilar insulin products in India, Brazil, and Southeast Asia.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/12070

Market Segment Insights

BY SYRINGE SIZE

0.5 mL (1/2 CC) Syringes: Dominant segment with 47.3% revenue share in 2025. Reflecting its role as the default specification for standard U-100 dosing regimens, accommodating doses up to 50 units in a single injection. Hospital formulary committees default to 0.5 mL syringes for inpatient insulin protocols, and this institutional inertia sustains the segment’s majority share.

1.0 mL (1 CC) Syringes: Fastest-growing size segment at 5.50% CAGR (2026–2035). Propelled by the growing use of concentrated U-500 insulin therapies for patients with severe insulin resistance requiring doses above 200 units daily. The ADA’s 2025 Standards of Care formally recommend concentrated insulin for this population, expanding the addressable U-500 syringe base.

BY DISEASE TYPE

Type 2 Diabetes: Dominant application with 85.0% share in 2025, representing the vast majority of the Insulin Syringes Market consumption because of its overwhelming prevalence. As Type 2 disease progresses, patients transition from oral medications to insulin therapy, creating a steady inflow of new syringe users.

Type 1 Diabetes: Fastest-growing disease segment at 5.50% CAGR. Driven by rising pediatric diagnoses and intensive insulin protocols requiring 4–6 daily injections. Though fewer in number, Type 1 patients generate higher per-patient syringe consumption, supporting premium demand.

BY END USER

Hospitals and Clinics: Largest segment at 51.0% share in 2025. Anchored by institutional procurement contracts and inpatient insulin management needs. Over 60% of U.S. hospital syringe procurement flows through three major GPOs, locking in multi-year volume commitments.

Home-Care Settings: Fastest-growing end-user segment at 5.60% CAGR. Reflecting patient preference for self-administration and telehealth-guided dosing. The COVID-19 pandemic permanently accelerated home-based insulin administration, and payers now incentivize self-management programs that reduce costly inpatient admissions. Diabetic injectable devices are among the most popular consumable categories on online pharmacy platforms, which handled over USD 75 billion in OTC and prescription sales in the United States in 2024.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/insulin-syringes-market-12070

Regional Outlook

North America — Dominant Market (~43% Share, 2025)

The United States generates approximately 72% of North American Insulin Syringes Market revenue, driven by Medicare/Medicaid coverage depth and entrenched GPO contracts. Over 60% of U.S. hospital syringe procurement flows through three major GPOs, locking in multi-year volume commitments. Reimbursement breadth and safety mandate compliance support premium-priced safety-engineered syringe demand that emerging markets cannot match.

Canada contributes through provincial formulary expansions at approximately 4.85% CAGR, while Mexico is growing on Seguro Popular insulin access mandates at USD 0.05 Billion in 2025. North America’s leadership rests on reimbursement depth and the structural safety-syringe segment created by OSHA mandates and expanded screening programs.

Europe — Second Largest (USD ~0.49 Billion, 2025)

Europe’s Insulin Syringes Market reflects divergent national strategies—Germany and the UK run universal statutory health insurance mandates, while Southern European markets rely more heavily on regional health authority procurement. Germany leads regionally with statutory health insurance mandates and a contribution of approximately 22% of regional share. The UK contributes at approximately 4.90% CAGR on NHS Long Term Plan diabetes provisions—the Plan has earmarked GBP 2.3 billion for diabetes care through 2029.

France contributes USD 0.08 Billion through social security reimbursement tiers. Italy contributes approximately 12% of regional share on regional health authority procurement. Spain contributes at approximately 4.55% CAGR on national diabetes strategy implementation. The Nordic countries contribute USD 0.04 Billion on high per-capita insulin consumption. Russia holds approximately 4.30% CAGR through import substitution policies. Harmonization pressure from EU MDR post-market surveillance requirements is gradually consolidating share toward BD, B. Braun, and Terumo, lifting baseline demand for compliant products across the region.

Asia-Pacific — Fastest-Growing Region (5.55% CAGR, 2026–2035)

Asia-Pacific is the engine of volume growth for the Insulin Syringes Market. China holds the largest regional share with National Essential Medicines List inclusion and a combined diabetes patient population exceeding 140 million, growing at a solid pace. India is growing at approximately 6.20% CAGR on the back of CDSCO device rules, biosimilar launches, and a diabetes population exceeding 77 million.

Japan contributes USD 0.06 Billion through aging population demand and universal coverage at steady growth. South Korea holds approximately 8% of regional share through National Health Insurance procurement. ASEAN economies show steep growth at approximately 5.80% CAGR on rising diagnosis rates and government subsidies. The rest of Asia-Pacific is growing at mixed development stages. The region’s combined 200+ million diabetes patient populations anchor the global volume base for insulin syringe demand.

Middle East & Africa — Emerging Opportunity (USD ~0.10 Billion, 2025)

The Middle East & Africa carries significant unmet need and therefore opportunity. Saudi Arabia leads the region with Vision 2030 healthcare investment, contributing approximately 25% of regional share. The UAE is growing at approximately 5.10% CAGR on medical tourism and premium healthcare infrastructure.

South Africa contributes USD 0.01 Billion on public hospital procurement. Egypt holds approximately 4.60% CAGR on population growth and rising diagnosis rates. The rest of MEA is growing on donor-funded diabetes programs, contributing approximately 30% of regional share. Gulf Cooperation Council states are investing heavily in diabetes infrastructure as part of national health transformation programs, with Saudi Arabia’s Vision 2030 directing over SAR 4 billion toward chronic disease management facilities. Sub-Saharan Africa remains dependent on WHO and donor-funded insulin programs, where syringe supply is bundled with insulin shipments.

South America — Growing Presence (~7% Revenue Share, 2025)

Brazil anchors South America’s Insulin Syringes Market at approximately 58% of regional revenue, with Sistema Único de Saúde (SUS) distributing insulin and syringes free of charge to registered diabetic patients, anchoring stable government procurement volumes that account for the majority of regional consumption. Argentina contributes at approximately 4.40% CAGR on provincial insulin distribution programs.

The rest of South America is growing on fragmented payer landscapes at USD 0.03 Billion in 2025. South America’s procurement runs largely through national public health systems, which pool demand to secure competitive pricing. The region’s stable demand base supports manufacturer volume planning even as per-unit tender prices compress margins. Biosimilar insulin launches across the region are expected to expand the addressable patient base significantly through 2035.

Competitive Landscape and Recent Developments

The Insulin Syringes Market exhibits medium concentration, with the top five players capturing an estimated 55–65% combined revenue share. Becton Dickinson holds a commanding position through its BD brand, while B. Braun, Terumo, and Nipro compete on safety-engineered product portfolios. The remaining market is fragmented across regional manufacturers, particularly in India and China, where cost-competitive producers serve government tender volumes. Concentration is highest in high-income segments where regulatory and manufacturing barriers are steep; the emerging-market tier is more fragmented as regional producers compete on price.

The competitive landscape is stratified between global safety-engineered leaders serving hospital and private markets, high-volume low-cost suppliers capturing government tender volumes, and integrated insulin manufacturers bundling syringes with vial kits.

KEY COMPANIES AND RECENT MILESTONES

Becton, Dickinson and Company (BD) (2024–2025): Maintains leadership with BD Ultra-Fine and BD Safety-Lok insulin syringes, commanding approximately 18–22% of global Insulin Syringes Market revenue. Global leader in safety-engineered insulin delivery. The company invested over USD 200 million in safety syringe manufacturing capacity between 2022 and 2024, signaling industry-wide commitment to the safety upgrade cycle.

Braun Melsungen AG (November 2024): Opened a new safety-syringe production line at its Penang, Malaysia facility, adding 500 million units of annual capacity to serve Asia-Pacific hospital tenders. Estimated revenue share: approximately 8–12%. European-market stronghold with MDR compliance focus.

Terumo Corporation (August 2024): Received FDA 510(k) clearance for its next-generation low dead-space insulin syringe, which retains less than 1 unit of residual insulin per injection. Estimated revenue share: approximately 7–10%. Asia-Pacific manufacturing scale leader.

Future Outlook: 2026–2035

By 2030, digital health integration and connected syringes will become the operating system of diabetes management. Bluetooth-enabled insulin syringe caps that log injection time, dose, and body site have entered pilot programs at three major U.S. health systems. Pairing syringe-level data with continuous glucose monitor feeds creates a closed-loop dosing record that payors can use for outcomes-based reimbursement, potentially lifting average selling prices 40–60% above standard syringe pricing. Major EHR vendors are already developing APIs for injectable device data, suggesting that connected syringes will become a reimbursement differentiator within the Insulin Syringes Market by 2030.

Sustainability-driven product redesign will reframe cost structures by the early 2030s. Extended producer responsibility frameworks expanding across Europe and Asia will push manufacturers toward recyclable polymers and reduced-plastic syringe barrel designs by 2030. Companies that achieve 20–30% material weight reduction without compromising sterility or structural integrity will capture procurement preference in markets where ESG scoring influences hospital purchasing. The European Parliament’s Extended Producer Responsibility directive for medical waste, adopted in late 2024, will require syringe manufacturers selling into the EU to fund the collection and incineration of used sharps.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/diabetes-devices-market-12288

https://www.marketresearchfuture.com/reports/insulin-delivery-devices-market-851

https://www.marketresearchfuture.com/reports/prefilled-syringes-market-6167

https://www.marketresearchfuture.com/reports/syringes-market-19219

https://www.marketresearchfuture.com/reports/injectable-drug-delivery-devices-market-1211

https://www.marketresearchfuture.com/reports/diabetes-monitors-market-4781

https://www.marketresearchfuture.com/reports/wearable-medical-device-market-899

https://www.marketresearchfuture.com/reports/drug-delivery-system-market-43638

https://www.marketresearchfuture.com/reports/home-healthcare-market-2030

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery